It usually starts with a quiet moment—standing in the kitchen after the kids have gone to bed, staring at a stack of mail you’ve avoided opening because everything suddenly feels uncertain. You’re not just ending a marriage; you’re trying to figure out how to protect the life you’ve built, the future you imagined, and the sense of security your family depends on. In that moment, Dividing a Pension in Your Divorce stops being a technical legal concept and starts feeling deeply personal, because the decisions you make now will echo for decades.

At The Law Office of Bryan Fagan, PLLC, we’ve walked alongside Texas families who never expected to be here but still want to move forward with clarity and dignity. Texas law treats retirement benefits earned during marriage as community property, and under Texas Family Code §153.002, courts are guided by what serves a child’s best interest—an interest that is closely tied to financial stability, predictability, and reduced conflict at home. When pension issues are ignored or misunderstood, they often lead to prolonged disputes, stress, and uncertainty that affect every corner of family life.

Founded by Bryan Joseph Fagan, a South Texas College of Law graduate and recognized authority on Texas divorce and custody law, our firm is built on a simple purpose: empowering people to reclaim freedom and peace of mind during life’s hardest transitions. In this article, you’ll learn how Texas courts approach pension division, why careful planning matters far beyond the courtroom, and how compassionate legal guidance can help protect what matters most—your future, your family, and your ability to move forward with confidence.

Key Takeaways

- Texas treats pensions earned during marriage as community property subject to division under Texas Family Code Chapter 7

- A Qualified Domestic Relations Order (QDRO) is required to legally divide most pension benefits—your divorce decree alone is not enough

- Only the marital portion of a pension is divisible; pre-marital and post-divorce service periods remain separate property

- Timing matters critically—delays in QDRO preparation can cost you retirement benefits if your spouse retires or dies before the order is approved

- Common mistakes like failing to address the pension in your decree or neglecting survivor benefits can permanently impact your financial security

Your Family’s Future Starts Here

Don’t navigate your legal journey alone. Schedule a consultation now and get the clarity and support you deserve.

Dividing a Pension in Your Divorce: The Big Picture

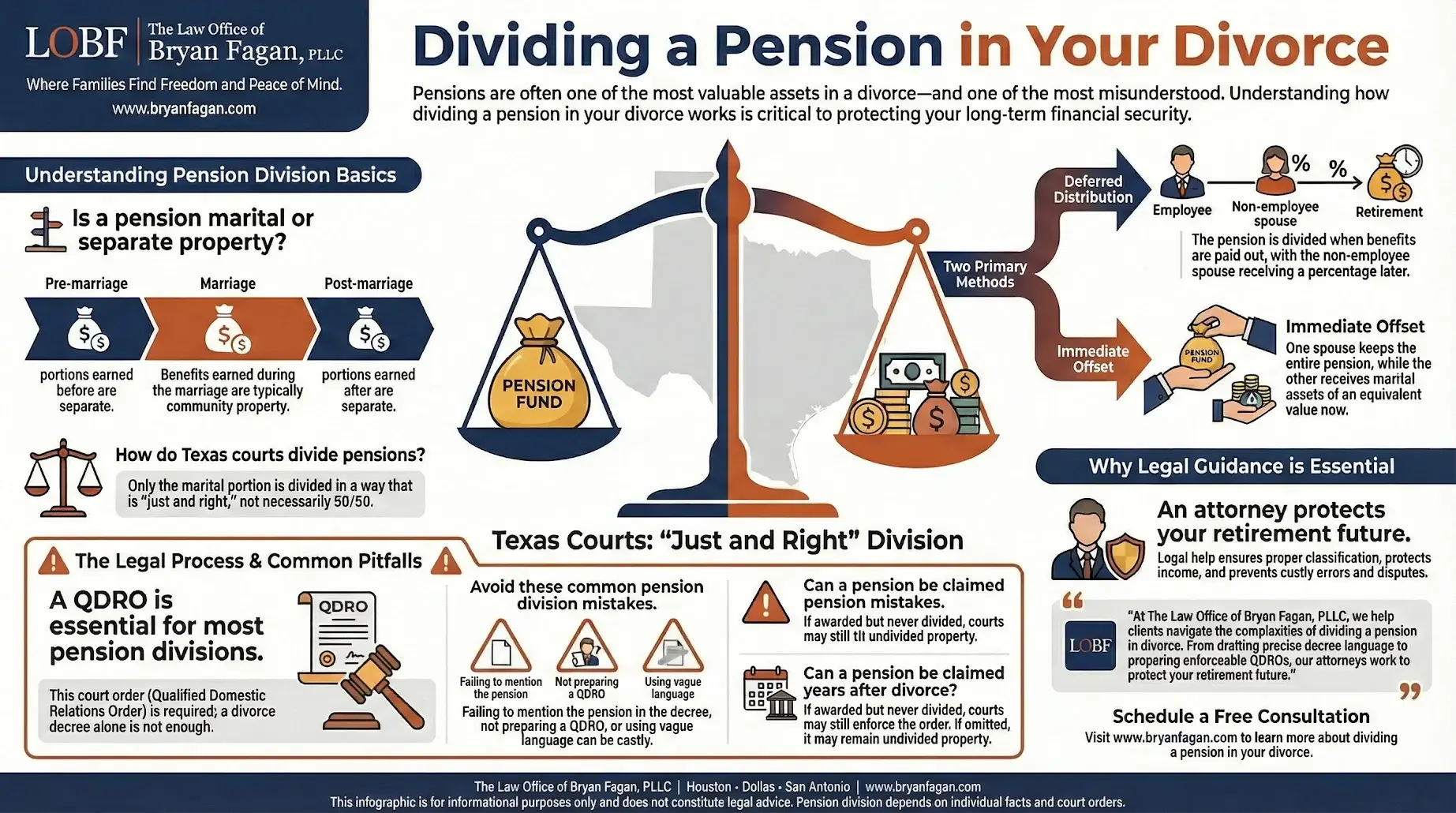

Under Texas law, Dividing a Pension in Your Divorce falls squarely within the state’s community property system, but retirement benefits require a more nuanced approach than dividing cash or household assets. Texas Family Code §3.002 creates a presumption that property acquired during marriage is community property, while §7.001 directs courts to divide that community estate in a manner that is “just and right.” Texas judges apply these statutes with particular care to pensions because they represent long-term financial security rather than immediate, spendable funds.

Pensions are uniquely challenging because they promise future income instead of providing a present balance that can be easily split. A defined benefit pension may not begin paying monthly benefits until years or even decades after the divorce. For that reason, Texas courts do not simply transfer money from one spouse to the other. Instead, they rely on deferred division methods—most commonly through a qualified domestic relations order or a comparable order for government plans—to divide benefits while avoiding unnecessary taxes and penalties. This process reflects both current Texas court practice and the Legislature’s intent to protect each spouse’s financial future.

The most important distinction in pension cases is that only the portion earned during the marriage is divisible. Under Texas Family Code §3.001, benefits accrued before the marriage or after the divorce is finalized remain separate property. That legal line makes accurate employment timelines, service credit records, and plan documents critical evidence. Without proper documentation, a spouse may unintentionally give up benefits they should keep or fail to claim benefits they are legally entitled to receive.

Attorneys with The Law Office of Bryan Fagan, PLLC regularly counsel families that pensions are often among the most valuable assets in a Texas divorce—sometimes even more valuable than the family home. Because pension payments feel distant and intangible, many people underestimate their importance or misunderstand how division works. Life events after divorce, such as remarriage, can also raise questions about ongoing pension rights, which is why understanding issues discussed in resources like whether remarriage affects an ex-spouse’s pension rights is so important. For readers who want a broader understanding of how Texas law treats retirement assets, our firm’s educational materials on divorce and retirement benefits in Texas provide additional guidance to help families move forward with clarity and confidence.

Is a Pension Community Property or Separate Property in Texas?

Texas courts determine the community portion of a pension by calculating the fraction of service credits earned during your marriage. Under Texas Family Code § 3.001, separate property includes assets acquired before marriage, while § 7.001 presumes that all property possessed during marriage is community property unless proven otherwise.

The practical application works like this: courts examine your date of hire, your marriage date, and your divorce date to calculate what percentage of your total pension service occurred during the marriage. If you worked for your employer for 30 years total, but only 20 of those years fell during your marriage, approximately 66.7% of your pension benefits would be classified as community property subject to division.

Pre-marital pension contributions remain your separate property if you can document them through employment records, vesting schedules, or pension statements. However, the burden falls on you to trace and prove these separate property claims. Texas case law, including Zisblatt v. Zisblatt (1995), emphasizes the importance of detailed documentation to rebut the community property presumption.

Post-divorce service is unequivocally separate property—your former spouse has no claim to pension benefits earned after your divorce is final. However, promotions or salary increases that occurred during the marriage may affect the calculation of the marital portion, even if the corresponding benefits won’t be paid until after divorce.

Why do dates matter so much? Errors in service date calculations can inflate or deflate the divisible amount by 20-50% based on service overlaps. Getting the timeline wrong could mean losing a significant portion of your retirement savings to your former spouse—or failing to claim benefits you’re legally entitled to receive.

How Texas Courts Divide Pensions in Divorce

Texas courts commonly rely on the “time rule” when Dividing a Pension in Your Divorce, particularly for defined benefit plans that pay monthly income at retirement. This approach aligns with Texas Family Code §7.001, which requires a “just and right” division of the community estate. Under the time rule, judges calculate the marital portion by comparing the years of service earned during the marriage to the total years of service, then apply that fraction to the accrued benefit. The resulting marital share is typically divided between the spouses based on fairness and the overall property division, rather than by an automatic formula.

Understanding the type of retirement plan involved is critical because Texas courts treat pensions differently depending on how they are structured. Defined benefit plans promise a future monthly payment based on salary and years of service, which means division usually occurs on a percentage basis and payments are deferred until retirement. Defined contribution plans, such as 401(k)s, are handled more directly because they have a specific account balance that can be valued and divided as of the date of divorce. These distinctions reflect Texas Family Code §3.001 and §3.002, which separate community property from a spouse’s separate property based on when and how the asset was acquired.

For defined benefit pensions, deferred distribution is the norm. The divorce decree awards the non-employee spouse a percentage interest, but actual payments begin only when the employee spouse retires and starts receiving benefits. While this method avoids immediate tax consequences and early withdrawal penalties, it can raise concerns about future events, including what happens if retirement is delayed or if a former spouse seeks to assert rights years later. Questions like these are addressed in greater detail in our firm’s resource on whether an ex-spouse can claim pension benefits years after divorce, which explains how Texas Family Code §9.201 governs enforcement and division of retirement assets that may have been overlooked or disputed after a decree is signed.

Survivor benefits also require careful attention during pension division. Without clear language in the divorce decree and any required retirement division order, the non-employee spouse may lose their entire interest if the employee spouse dies before or shortly after retirement. Texas courts often address this risk by requiring joint-and-survivor annuity elections or other protective measures to ensure the awarded share is meaningful and enforceable. Attorneys with our Texas family law team frequently emphasize that these provisions are not optional details but essential safeguards for long-term financial security.

A practical example often helps bring these concepts together. If a teacher worked for 25 years and 18 of those years occurred during the marriage, approximately 72 percent of the pension would be classified as community property. If the court then divides that marital portion equally, the non-employee spouse would receive 36 percent of each monthly benefit when retirement begins. Scenarios like this highlight why careful planning and informed legal guidance matter so much when retirement assets are on the line, and why families benefit from reviewing trusted educational resources such as our broader discussions on Texas divorce and retirement benefits before finalizing any agreement.

What Is a QDRO and Why Is It Required?

A Qualified Domestic Relations Order (QDRO) is a specialized court order that creates or recognizes an alternate payee’s right to receive a portion of a participant’s pension benefits. Under federal law (ERISA, 29 U.S.C. § 1056(d)), private employer pension plans cannot pay benefits to anyone other than the plan participant without a valid QDRO approved by the plan administrator.

Here’s what many divorcing spouses don’t understand: your divorce decree is not enough to divide a pension. The decree establishes the court’s intent—for example, that you should receive 50% of the marital portion of your spouse’s pension. But pension plan administrators are not parties to your divorce. They follow federal ERISA rules, not state court orders.

The QDRO bridges this gap by providing the specific mechanics the plan administrator needs:

- Exact percentages or dollar amounts

- Payment timing and conditions

- Addresses for both parties

- Survivor benefit elections

- Early retirement subsidy treatment

Without an approved QDRO, the pension plan administrator will reject any request to divide benefits. Your right to pension funds exists only on paper until the QDRO is submitted, reviewed, and approved.

Texas Family Code § 9.101 authorizes courts to enter QDROs as part of divorce proceedings or afterward. However, the QDRO must conform to the specific pension plan’s requirements. A QDRO that works perfectly for one employer’s plan may be rejected by another. This is why experienced divorce attorneys often coordinate with QDRO specialists who understand model QDROs and plan-specific requirements.

It’s worth noting that QDROs apply specifically to ERISA-covered plans. IRAs can be divided through a “transfer incident to divorce” under IRS rules without a QDRO, avoiding early withdrawal penalties through different mechanisms.

Timing Issues When Dividing a Pension in Your Divorce

QDROs are frequently prepared and submitted after the divorce decree finalizes because most pension plans require the final decree before they will review and approve a QDRO. This creates a gap between when your divorce ends and when your pension division becomes legally enforceable against the plan.

This timing gap carries significant risk. If the employee spouse retires before the QDRO is approved, payments may begin flowing solely to them—requiring retroactive court orders to recover the non-employee spouse’s share. If the employee spouse dies before the QDRO is in place, the non-employee spouse’s claim may be completely extinguished unless the divorce decree specifically preserved survivor benefits through other means.

Texas Family Code § 9.201 allows post-decree QDRO enforcement, but practical challenges multiply with every month of delay. Plan administrator approval typically takes 30-90 days, assuming the QDRO is properly drafted. If revisions are needed, the process starts over.

Best practices for protecting your pension rights include:

- Draft QDRO language into your divorce decree for seamless transition

- Submit the QDRO to the plan administrator within 60 days of divorce finalization

- Request pre-approval review of draft QDRO language before finalizing your divorce

- Include temporary orders protecting pension benefits during divorce proceedings

Studies of Texas divorce practices suggest that 30% or more of delayed QDROs result in lost benefits, with some cases involving losses exceeding $100,000 in present value.

Common Mistakes When Dividing Pensions in Divorce

Failing to mention the pension in the divorce decree is perhaps the most costly mistake divorcing spouses make. If the pension is omitted from your property division, you may forfeit your claim to share in retirement benefits your spouse earned during your marriage. Texas Family Code § 9.201 provides some recourse for omitted property, but pursuing these claims after divorce is expensive and uncertain.

Assuming the pension belongs solely to the employee spouse ignores Texas community property law. Regardless of whose name appears on the pension plan, benefits earned during marriage belong to both spouses. The non-employee spouse’s contributions—whether through household management, childcare, or career sacrifices—support the family’s overall financial growth, including retirement savings.

Not securing survivor benefits exposes the non-employee spouse to catastrophic loss. Without proper QDRO language requiring survivor benefit elections, the non-employee spouse receives nothing if the employee spouse dies before or shortly after retirement. This isn’t just a theoretical risk—it happens regularly to spouses who didn’t understand what they were signing.

Using vague or incorrect legal language in the divorce decree prompts plan rejections. Phrases like “fair share” or “equitable portion” mean nothing to a pension plan administrator. QDROs require specific percentages, dates, and payment mechanics. Imprecise language can delay division for months or years.

Delaying QDRO preparation invites tax complications, plan changes, and the risks described above. Every month without an approved QDRO is a month where your pension rights remain unprotected.

The financial consequences are severe. Case studies from Texas divorces show these errors reduce retirement income recoveries by 40-70%, with litigation costs averaging $15,000 or more to correct preventable mistakes.

What Happens If a Pension Was Omitted From the Divorce?

When a retirement benefit is overlooked during divorce, Dividing a Pension in Your Divorce often becomes far more stressful and expensive after the decree is signed. Texas law treats an unintentionally excluded pension as “omitted marital property” under Texas Family Code §9.201, which allows a former spouse to ask the court to divide that asset even after the divorce is final. While this statute provides a safeguard against unfair outcomes, it also underscores why Texas courts expect retirement benefits to be identified and addressed clearly during the original divorce proceedings.

Strict deadlines apply to these post-divorce claims. In most cases, a spouse has two years from the date the divorce decree was signed to seek division of omitted property. If fraud is alleged, the limitations period may instead run from the date the fraud was discovered rather than the decree date. Courts require evidence that the pension was omitted unintentionally and that the parties never previously agreed to divide or waive the asset. These issues—and whether a former spouse can still assert pension rights years later—are explained in detail in whether a wife can claim a pension years after divorce, which walks through how Texas courts analyze delayed pension claims.

Texas law does not usually require reopening the entire divorce case to address an omitted pension. Instead, courts may resolve the matter through clarification or enforcement proceedings that focus solely on the missing retirement asset. That said, equitable defenses such as laches—an unreasonable delay that prejudices the other party—can bar recovery if a spouse waits too long after discovering the omission. Acting promptly and preserving documentation are essential to protecting pension rights under the current Texas Family Code framework.

Texas appellate courts have consistently recognized the authority to divide omitted pensions when the evidence supports their classification as community property. In Hollis v. Hollis (2010), for example, the court upheld pension division years after divorce where the asset clearly belonged to the community estate. Even with favorable case law, attorneys with our Texas family law team routinely caution that post-divorce pension litigation is far more costly and uncertain than addressing retirement benefits correctly from the outset. For families looking to avoid these complications and better understand their options, our educational resources on Texas divorce and retirement planning provide additional guidance to help protect long-term financial security.

Tax and Financial Considerations When Dividing a Pension

When Dividing a Pension in Your Divorce, it is essential to understand how taxes follow the money, not the person who earned it. Under federal tax law, pension payments received by either spouse pursuant to a properly executed qualified domestic relations order are taxed as ordinary income to the recipient. In practical terms, if you are awarded 40 percent of your former spouse’s pension, you—not your former spouse—are responsible for paying income taxes on that 40 percent. Texas Family Code §7.001 reinforces the importance of handling this division carefully by requiring a “just and right” allocation of community property, which necessarily includes awareness of post-divorce tax consequences.

One of the most significant advantages of using a properly drafted QDRO is that it avoids the 10 percent early withdrawal penalty that normally applies to retirement distributions taken before age 59½. The QDRO exception allows the non-employee spouse to receive their share of pension benefits without triggering that penalty, even if they are younger than the typical retirement age. QDRO distributions also avoid the mandatory 20 percent federal withholding that often applies to other types of retirement plan payouts, making them a more efficient tool when dividing retirement benefits under Texas law.

It is also important to recognize that pensions are taxed differently than other retirement assets commonly addressed in divorce. With defined contribution plans such as 401(k)s or IRAs, funds can often be transferred tax-free into another retirement account, deferring taxes until withdrawals occur later. Defined benefit pensions do not offer this flexibility. Instead, taxes are paid gradually, as monthly annuity payments are received. This distinction often surprises families and underscores why careful planning matters when retirement benefits make up a substantial portion of the marital estate.

Attorneys with our Texas family law team frequently encourage clients to coordinate pension decisions with qualified financial and tax advisors during settlement negotiations. Trading pension rights for assets like home equity or cash may seem appealing, but those decisions require accurate present value calculations. Actuarial experts routinely find valuation differences of 25 to 35 percent depending on assumptions about life expectancy, retirement age, and cost-of-living adjustments. Misjudging those numbers can mean giving up far more long-term retirement income than intended, particularly in cases involving public safety pensions such as firefighter benefits, which are discussed in greater detail in how firefighter pensions are divided during divorce.

Long-term financial security depends on understanding both the legal and tax consequences of pension division. An uncoordinated approach can easily create tens of thousands of dollars in avoidable lifetime tax disadvantages, undermining the stability Texas courts aim to protect when dividing community property. For families seeking a deeper understanding of retirement planning in divorce, our educational materials on Texas divorce and retirement benefits offer additional guidance to help protect what matters most while planning for the future with clarity and confidence.

How a Texas Divorce Attorney Protects Your Pension Rights

Protecting retirement benefits requires far more than filling out forms, which is why Dividing a Pension in Your Divorce is best handled with experienced legal guidance. A seasoned Texas divorce attorney safeguards pension rights through thorough discovery, careful drafting, and forward-looking strategy. Retirement benefits are often among the most valuable assets in a marriage, and the technical requirements for dividing them correctly leave little room for error. Attempting to handle these issues without professional support can result in permanent financial consequences that are difficult or impossible to fix later.

During the discovery phase, an attorney ensures that all retirement assets are identified and disclosed as required by Texas Family Code §6.502. This process goes well beyond obvious pensions and includes 401(k) plans, IRAs, deferred compensation, and employer-sponsored retirement benefits that a spouse may not even realize exist, especially when multiple employers or long careers are involved. Complete and accurate discovery lays the foundation for a fair division under Texas Family Code §7.001, which requires a “just and right” distribution of community property.

Precise drafting in the divorce decree is equally critical. Legal counsel ensures the decree clearly addresses how the marital portion of the pension will be calculated, how survivor benefits will be handled, who is responsible for preparing and submitting any required qualified domestic relations order, and what protections apply while that order is pending approval. These details are not mere technicalities; they are the safeguards that prevent future disputes and enforce the court’s intent. Questions about whether a pension must be shared at all are explored more fully in whether a spouse must share a pension in a Texas divorce, which explains how Texas law distinguishes between community and separate property.

Experienced family law attorneys also coordinate closely with QDRO specialists and plan administrators to ensure retirement division orders comply with both Texas law and the specific requirements of each pension plan. This collaboration helps avoid rejections, delays, or unintended loss of benefits. Just as important, legal counsel anticipates life changes that can affect retirement benefits, such as early retirement, disability, job loss, or death, and builds protections into the decree to address those possibilities before they become costly problems.

Understanding the full process of pension division requires more than legal knowledge; it requires practical experience guiding families through complex transitions. Attorneys with our Texas family law team focus on education and clarity, helping clients understand their rights while protecting long-term financial security. For readers seeking additional insight into retirement issues in divorce, our broader resources on Texas divorce and retirement benefits offer further guidance designed to help families move forward with confidence and peace of mind.

Why Choose The Law Office of Bryan Fagan, PLLC

Guiding families through Dividing a Pension in Your Divorce requires more than technical knowledge—it calls for experience, foresight, and a genuine commitment to protecting long-term stability. Attorneys with our Texas family law team bring extensive experience handling retirement asset division under Texas Family Code Chapter 7, including §7.001’s requirement that courts divide community property in a manner that is “just and right.” Having helped hundreds of Texas families navigate divorce, our focus remains on safeguarding retirement security while minimizing uncertainty and conflict.

A thoughtful, detail-oriented strategy is central to how pension cases are handled. Each situation involves a careful review of employment histories, service timelines, and plan-specific rules to determine what portion of the benefit qualifies as community property under Texas Family Code §§3.001 and 3.002. When valuations become complex, legal counsel often collaborates with QDRO specialists, financial advisors, and actuaries to ensure that division methods are accurate, enforceable, and aligned with both state law and plan requirements.

Clear communication and compassionate guidance shape every client relationship. Dividing retirement benefits is rarely just a legal exercise; it is a deeply personal process that affects financial security for decades. Clients are guided through each option in plain language, with careful explanations of how today’s decisions may affect tomorrow’s peace of mind. For those seeking a broader understanding of what to expect along the way, our resource on the Texas divorce process explained step by step offers helpful context and education.

Families across Texas—from large metropolitan areas to smaller communities—turn to our firm for steady guidance during difficult transitions. No matter where a pension plan is administered or where a family is located, the goal remains the same: to educate, empower, and protect what matters most. With informed legal support and a clear strategy, families can move forward with confidence, knowing their retirement future has been thoughtfully addressed.

Checklist: Dividing a Pension in Your Divorce

Use this checklist to protect your retirement benefits during divorce:

- [ ] Identify all pension and retirement plans held by either spouse

- [ ] Gather employment records showing hire dates and service periods

- [ ] Determine which service dates fall within the marriage

- [ ] Obtain current pension statements and plan summary documents

- [ ] Ensure the pension is explicitly addressed in the divorce decree

- [ ] Include specific language about survivor benefits and QDRO preparation

- [ ] Prepare and submit the QDRO within 60 days of divorce finalization

- [ ] Follow up with the plan administrator to confirm approval

- [ ] Consult an experienced Texas divorce attorney before finalizing any division

Conclusion

Divorce has a way of forcing big decisions into moments when clarity feels hardest to find. Questions about money, parenting, and the future tend to blur together, and it’s easy to underestimate how one choice—like how a pension is divided—can shape everything that comes next. What matters most is knowing that these decisions don’t have to be made in isolation or under pressure. With the right guidance, even complex issues can become manageable, and uncertainty can give way to confidence.

At The Law Office of Bryan Fagan, PLLC, we believe education is a form of empowerment. When you understand your rights and options under Texas law, you’re better equipped to protect your financial stability, reduce conflict, and create a healthier path forward for your family. Working with an experienced Texas family law attorney means having someone who not only understands the legal landscape but also appreciates the human side of what you’re going through.

If you’re facing divorce and wondering how today’s decisions will affect your life years from now, consider taking that next step—whether it’s scheduling a consultation, asking questions, or simply learning more before you act. The future doesn’t have to feel overwhelming. Sometimes, peace of mind begins with one informed conversation and the reassurance that you don’t have to navigate this transition alone.

Frequently Asked Questions

In Texas, pensions are divided based on the portion earned during the marriage because Texas is a community property state. Courts typically use a “time rule” formula that compares the years of service during the marriage to the total years of service. Only the marital portion is subject to division, and the split must be “just and right,” not automatically equal. Most pensions require a separate court order—often a Qualified Domestic Relations Order (QDRO)—to actually carry out the division.

One of the biggest mistakes people make is focusing only on short-term outcomes and overlooking long-term consequences. Retirement assets like pensions are easy to ignore because they don’t feel immediate, but they are often among the most valuable assets in a divorce. Another common mistake is failing to complete the paperwork needed to enforce the division, which can result in lost benefits years later.

In many cases, the portion of the pension earned during the marriage is considered community property under Texas law. Even if only one spouse worked outside the home, both spouses are considered to have contributed to the marriage. A court may award your ex-wife up to half of the marital portion as part of an overall property division, but this does not usually include benefits earned before marriage or after divorce.

Not automatically. Texas courts divide only the marital portion of the pension, not the entire benefit. The actual percentage your ex-wife receives depends on how long you were married, how long you worked for the employer, and how the court divides the overall community estate. Many cases result in something close to a 50/50 split of the marital portion, but that outcome is not guaranteed.

You may be entitled to a share of the portion earned during the marriage, but that does not necessarily mean half of the entire pension. Texas courts look at the full financial picture and divide community property in a way they consider fair. Factors like service dates, plan type, and other assets awarded in the divorce can all affect the final outcome.

Separate property is generally not divisible in a Texas divorce. This often includes assets owned before marriage and certain gifts or inheritances received by one spouse. However, separate property must usually be proven with clear documentation. If funds were mixed with community money or used for marital purposes, they may lose their separate character and become subject to division.

The “10 10 10 rule” is not an official Texas divorce rule. Some people use it as a mindset tool, asking how they will feel about a decision in 10 days, 10 months, and 10 years. Others confuse it with military retirement rules, often called the “10/10 rule,” which relates only to how military retirement payments are made—not whether the pension can be divided. If someone mentions a “10 10 10 rule” in your case, it’s important to clarify what they mean.

There isn’t a universal answer. Higher earners may lose more on paper through property division or support obligations, while lower earners may feel the financial impact more acutely due to income gaps and higher living costs post-divorce. Retirement assets like pensions can significantly affect who feels the financial strain, especially if they are mishandled or ignored during the divorce process.

The “7 7 7 rule” is a relationship concept, not a legal rule. It’s often described as spending intentional time together regularly, such as a date every seven days, an outing every seven weeks, and a trip every seven months. While it doesn’t apply to divorce law, the underlying idea—intentional communication and consistency—can be helpful for co-parents trying to reduce conflict and create a more stable post-divorce family environment.