Managing a trust for a loved one with disabilities requires both compassion and precision. When you serve as trustee of a special needs trust under Texas law, understanding the distribution rules is essential to protect the beneficiary’s eligibility for government benefits while using trust funds to enhance their quality of life. Now, we’ll focus squarely on the distribution-rules side of a Texas special needs trust, exploring when, how, and for what purposes you may make disbursements while aligning with both federal and Texas requirements.

Let’s discuss what trustees need to know: from baseline eligibility and trust types, to specific distribution practices, to oversight and decision-making. As you move through the sections below, you’ll gain clarity on your duties, permissible uses of funds, monitoring concerns, and strategies to optimize benefit preservation.

Understanding the Basics of a Texas Special Needs Trust Distribution Rules

Before you issue payments from the trust, you must understand the structural rules of the trust itself and how distribution rules operate under federal and Texas frameworks. When focusing on Texas special needs trust distribution rules, you must concentrate on how payout decisions tie into compliance.

- Type of trust matters. Under federal law, a first-party (or “self-settled”) special needs trust (often a § 1917(d)(4)(A) trust) must be irrevocable, established for a beneficiary under age 65 at funding, with a Medicaid pay-back provision at the beneficiary’s death. A third-party trust is funded by someone other than the beneficiary and typically has no Medicaid pay-back requirement.

- Eligibility-preserving objective. The primary goal is to allow the beneficiary to remain eligible for federal and state benefits (such as Supplemental Security Income (SSI) and Medicaid) while funds in the trust are used to supplement, and not supplant, their needs.

- Trust drafting and terms. In Texas, there is no statute that prescribes one specific form for a special needs trust; however, proper wording, discretionary distribution authority, and a spendthrift clause are common features to satisfy federal benefit eligibility standards.

- Resource and income rules. The federal SSI program treats many trust distributions differently depending on how they are paid. For example: cash to a beneficiary may count as unearned income; distributions for food or shelter may affect benefits as “in-kind support and maintenance (ISM).”

- Distribution rule focus. The trustee should also pay close attention to how distributions are made (to whom, for what purpose, how documented) and whether those distributions might trigger loss or reduction of benefits.

Planning and Executing Distributions Without Jeopardizing Benefits

Once you understand the framework, you must implement a distribution strategy that aligns with the accepted rules.

Establishing a Distribution Policy

- Draft a spend-down or spending plan. Work with a planner and attorney to determine anticipated needs of the beneficiary (immediate and long-term). This helps you decide how much, when and in what form distributions should be made.

- Define discretion. Ensure the trust grants you broad discretion to make distributions for “supplemental” purposes. A rigid formula may increase risk of mis-use.

- Prioritize benefit protection. Plan distributions so that you avoid converting trust assets to “countable” resources for benefit eligibility and avoid creating unearned income for the beneficiary.

Permissible vs Problematic Distributions

Under Texas-relevant trust planning, here’s how the distribution rules guide decisions:

Permissible distributions (when properly executed):

- Items and services beyond what the beneficiary’s government benefits cover–such as assistive equipment, therapies not covered by Medicaid, recreation, computer or adaptive technology.

- Payment of bills or services directly to vendors or providers rather than giving cash to the beneficiary. Many sources emphasize that if you purchase an item for the beneficiary rather than giving cash, you reduce risk of benefit loss.

- Home modifications, adaptive vehicles, travel, enrichment, hobbies–so long as the trust terms allow and benefit eligibility is preserved.

Problematic distributions under the rules:

- Cash payments or gift cards to the beneficiary, which are treated as direct income.

- Distributions that pay for “basic food or shelter” in a way that counts as ISM under federal rules. For example, paying rent or giving cash for groceries may reduce SSI benefits.

- Distributions that exceed the trustee’s authority under the trust agreement, or are not documented as for the beneficiary’s supplemental needs.

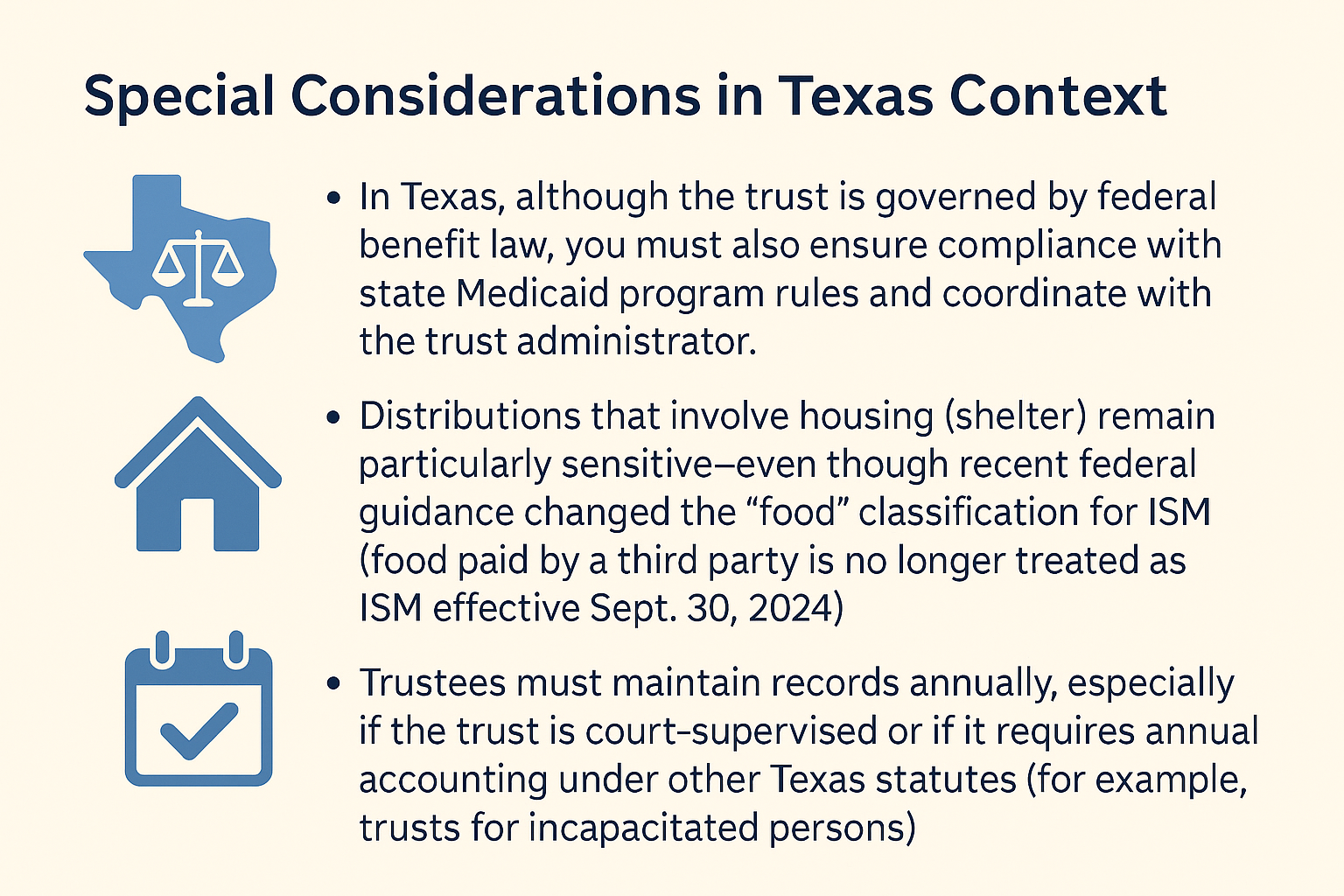

Special Considerations in Texas Context

- In Texas, although the trust is governed by federal benefit law, you must also ensure compliance with state Medicaid program rules and coordinate with the trust administrator.

- Distributions that involve housing (shelter) remain particularly sensitive—even though recent federal guidance changed the “food” classification for ISM (food paid by a third party is no longer treated as ISM effective Sept. 30, 2024).

- Trustees must maintain records annually, especially if the trust is court-supervised or if it requires annual accounting under other Texas statutes (for example trusts for incapacitated persons).

Sample Distribution Checklist

When evaluating a payout request, ask:

- Is this distribution for the sole benefit of the beneficiary, and in furtherance of the trust’s purpose?

- Will the trust pay the vendor directly (rather than giving cash to the beneficiary)?

- Does this payment risk being treated as food or shelter in benefit terms (thus triggering ISM)?

- Is it consistent with the trust document’s terms?

- Is proper documentation available (invoice, contract, vendor receipt)?

- Will this distribution unduly reduce the trust’s ability to serve future needs?

- Has the trustee considered tax consequences (trust income tax, beneficiary tax)?

Oversight, Monitoring and Adjusting for Long-Term Success

A key part of the Texas special needs trust distribution rules is not just making individual distributions, but overseeing the trust’s long-term administration so that distributions remain compliant and effective.

Trustee Duties Related to Distributions

- Duty of loyalty and prudence. Ensure trust funds are invested and disbursed in a way that supports the beneficiary. The trustee must manage assets with care.

- Duty to comply with trust terms and law. Your distribution decisions must reflect the trust instrument’s provisions and applicable law (benefit eligibility rules, federal and state).

- Record-keeping and accounting. Keep detailed records of each distribution: amount, date, recipient, purpose. This is particularly necessary if the beneficiary’s benefits agency audits or reviews.

- Review and adjust over time. The beneficiary’s needs may change (medical, educational, housing). Regularly revisit the spending plan and distribution strategy to reflect shifts in needs and in law.

Evaluating Benefit Risk When Distributing Funds

- When you make a distribution, consider whether it is likely to count as “income” or “resource” under SSI or Medicaid rules in Texas. For example, even if you pay directly to a vendor, if it effectively replaces benefits the government would otherwise cover, eligibility could be at risk.

- Use interaction with other tools wisely. For instance, an ABLE account (for eligible persons) may be used alongside the trust for certain expenses—this may affect distribution strategy under Texas planning.

- Given changing rules, such as the federal change eliminating food from ISM treatment effective Sept. 2024, keep up with benefit-agency guidance.

Preparing for Termination or Remainder Distributions

Eventually, a trust may wind down or distribute remaining assets (for example at the beneficiary’s death or under the trust terms). The “distribution rules” extend to how you handle final payouts. For instance:

- First-party trusts must satisfy Medicaid pay-back before remnant amounts go elsewhere.

- Ensure the trust’s language specifies how residual funds are handled (in a third-party trust) and that the distribution aligns with any remainder-beneficiary provisions.

- Maintain clean records so that final audits or reviews by state agencies can be completed without jeopardizing benefit eligibility or exposing you to liability.

Making Strategic Distribution Choices

Let’s look at how you as a trustee execute the Texas special needs trust distribution rules toward meaningful decisions and strategic outcomes for your beneficiary.

Balancing Immediate Needs and Long-Term Preservation

As trustee, you face choices: Should you distribute now to enhance life experiences, or preserve capital for future unknowns? For example:

- If the beneficiary would benefit from travel, enriched equipment, or adaptive housing upgrades, you might decide a distribution now will improve quality of life and not jeopardize benefits.

- If the beneficiary’s long-term care needs might increase (e.g., needing residential care, more intensive therapy in later years), you may hold back some resources.

- Document your rationale for distributions and reserved funds—this shows prudence.

Implementing a Budget-oriented Distribution Process

- Develop an annual budget for the trust: expected distributions and projected trust investment returns.

- Align distributions with the budget and trust terms—so you avoid ad-hoc payouts that may look unreasonable to benefit agencies.

- Consider establishing a distribution committee or advisory role (especially in a family context) to provide oversight and accountability.

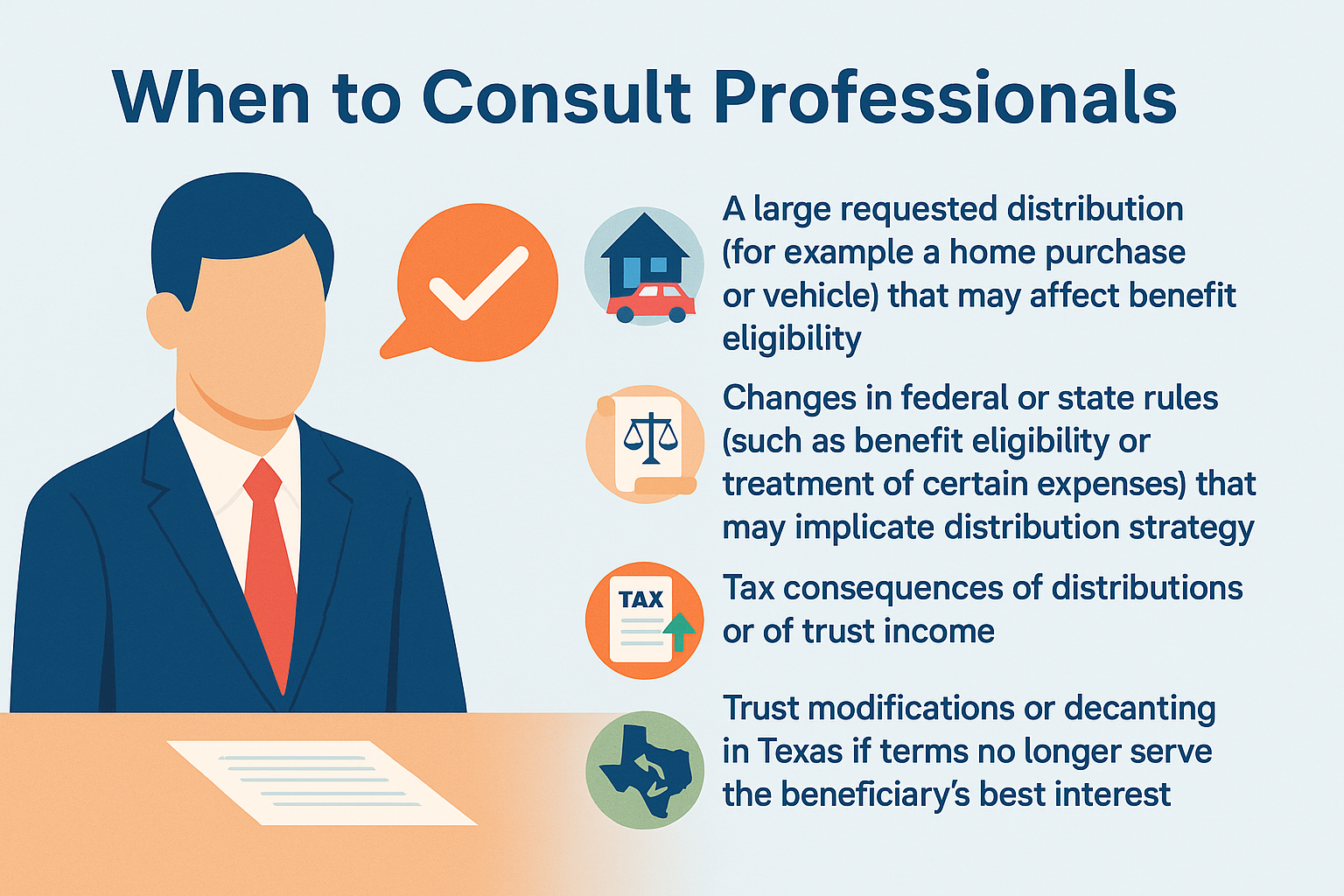

When to Consult Professionals

There are situations demanding professional input:

- A large requested distribution (for example a home purchase or vehicle) that may affect benefit eligibility.

- Changes in federal or state rules (such as benefit eligibility or treatment of certain expenses) that may implicate distribution strategy.

- Tax consequences of distributions or of trust income.

- Trust modifications or decanting in Texas if terms no longer serve the beneficiary’s best interest.

Succession Planning and Transition of Trusteeship

As trustee, you also need to think about the future:

- Ensure successor trustees are named and have training or information about special needs trust distribution rules.

- Provide the successor with documentation: trust instrument, spending plan, budget, distribution history, vendor contracts.

- On transition, consider a hand-off meeting or memo to ensure continuity and respect for the trust’s purpose.

Conclusion

Serving as trustee of a special needs trust in Texas demands a thoughtful focus on distribution rules. By thoroughly understanding how the trust must operate, planning distributions in light of government benefit eligibility, maintaining diligent oversight, and making strategic decisions with the beneficiary’s long-term welfare in mind, you can fulfill your role with confidence and care. The Texas special needs trust distribution rules may sound technical, but it really points to a practical promise: that the trust’s funds will be used wisely, enhancing the beneficiary’s life without jeopardizing essential benefits.

Other Related Posts

- Why You Need an Attorney for Living Will Decisions and Planning

- Finding the Right Texas Special Needs Trust Lawyer for Your Family’s Future

- Is a Living Will Legally Binding and How It Works in Real Situations

- Key Benefits of Minor Guardianship in Texas: Legal Protection and Parental Support

- Creating a Living Will: A Clear Legal Framework for Your Future Care

- How to File for Temporary Guardianship the Right Way: What You Need to Know

- Understanding the Cost of Special Needs Trust for Long-Term Planning

- How to Set Up a Living Will: Step-by-Step Legal Planning Guide

- Texas Guardianship Attorney Services: Essential Legal Support for Families

- Special Needs Trust Medicaid Guide: Protecting Benefits Without Sacrificing Support

- dvance Directives vs Living Will: A Practical Comparison for Medical Planning

- Texas Court Guardianship Evaluation Process: How It Works and What to Expect

Frequently Asked Questions

No. Distributions of cash to the beneficiary typically count as unearned income and may reduce or eliminate benefits such as SSI. Best practice: pay vendors directly or purchase goods/services for the beneficiary.

That is highly risky. Distributions that pay for shelter may be treated as “in-kind support and maintenance,” which reduces SSI benefits by a portion of the federal benefit rate.

Maintain documentation for every distribution: date, amount, recipient/vendor, purpose, beneficiary benefit, trust fund source. These records help prove compliance if audited.

First evaluate: Does the trust instrument permit the expenditure? Will it negatively impact benefits? Is it consistent with the spending plan and long-term preservation? Consult advisors if needed.

In a first-party trust, the remaining funds after the beneficiary’s death must reimburse Medicaid for medical assistance paid on their behalf, before any other distributions.